Unless you have a crystal ball, you probably don’t know exactly when you’re going to die. Luckily, you can buy a life insurance to provide a financial safeguard for your loved ones, should the worst happen and you pass away unexpectedly.

Buying *the right* life insurance policy can be a little confusing though. With so many coverage types and sneaky insurance sales reps slinging expensive policies with vociferous techniques, it’s hard to know what to buy and how much.

In this post, we’re going to boil down life insurance to the basics. You’ll learn the different types, what to avoid and what you might need, as well as cover the process of how to buy life insurance.

Talking about death can be weird (especially your own death!). But you shouldn’t ignore this uncomfortable yet important task. Failing to do so could leave your loved ones struggling to manage finances without you.

OK, let’s get started! 👇

The Basics of Life Insurance:

Think of life insurance like a legal promise… You make small annual payments to an insurance company, and in return, they promise to give your loved ones a big chunk of money if you die unexpectedly.

The big chunk of money is called a “death benefit.” You get to decide how much it is when you buy a policy (we’ll help you calculate a good coverage amount later in this post). And the loved ones that get the money are called “beneficiaries.” These can be family, friends – or really anyone you want to name, as long as they are a human (sorry dog lovers, you can’t leave money to pets!)

When you buy a life insurance policy, the goal isn’t to cheer people up with a big consolation prize if you die (no amount of money can take away sad feelings). Instead, policies are designed to cover specific financial costs.

The money can help with things like:

- Funeral expenses: Taking care of burial costs, travel or hosting a memorial service.

- Bills and everyday living: Helping your family stay afloat financially if you are the current breadwinner.

- Debts: Paying off any loans, mortgages, or repayments so that your loved ones don’t get stuck with a burden.

- Education: Funding your children’s college education, or maybe grandchildren.

- Savings: Leaving a legacy for your loved ones.

Important note: Although you might have a plan for how death benefit money should be spent, the people who receive the money can actually decide to spend it however they please. So when you buy life insurance it’s really important to a) choose beneficiaries that you trust, and b) involve them in discussions around how/why you set up the policy.

Different Types of Life Insurance

There are a handful of different life insurance products people can buy. But honestly, the vast majority of folks should only be concerning themselves with one type: Term Life Insurance. Almost all other insurance products are overkill (pun intended).

Here’s a quick and basic overview of different life insurance types…

| Policy Duration | Death Benefit | Cash Value | Premium Cost | |

| Term Life | Set term, usually 10-30 years | Yes | No | Lowest |

| Whole Life | Lifetime | Yes | Yes | Highest |

| Universal Life | Lifetime | Yes | Yes | Moderate |

| Variable Universal Life | Lifetime | Yes | Yes | Highest |

Term Life Insurance

These are the simplest and most cost effective life insurance policies available to buy. They are called “term” policies because they are put in place for a predetermined amount of time. Typically between 10 – 30 years.

Your beneficiaries will only receive the death benefit if you die while the policy is still active. In most cases, your death benefit remains the same throughout the policy term, meaning that the payout amount would be the same if you died in the first year of your policy, or your last!

What about after the term ends? Don’t I still need a policy? Well, even though lifelong coverage may sound appealing, the goal is to eventually build enough wealth in life so that you don’t need insurance at all. Self-insuring is the goal after a few decades.

In other words, as you keep saving and stuffing money into your retirement accounts, your personal nest egg grows bigger and bigger to the point where your loved ones will receive a bulky inheritance if you die anyway. As you grow older and wealthier, the need for insurance shrinks.

Believe me, 30 years is definitely enough time to build a significant nest egg. But, laddering policies is another way to extend coverage beyond just a 30-year timeline if you feel like coverage is needed for an even longer span of time.

Whole Life Insurance

Whole life insurance is a permanent policy, meaning you will keep paying policy premiums forever and ever. It’s the most expensive type of life insurance to buy, and it has very limited flexibility.

The main difference is in addition to a death benefit, there is also a slow growing “cash value” to your policy. This is essentially an investment-like savings account that grows slowly over time by a fixed interest rate. (Don’t get too excited, it’s typically a really really small interest rate!)

In exchange for your *much-higher* monthly premiums, the insurance company sets aside a tiny bit of money into a cash value account. The selling point here is that you are building savings over time, and you can borrow or withdraw money from your cash value later if you need it.

While this might all sound nice, whole life insurance policies are rarely a good deal. They are riddled with advisor fees and commissions, lock you into a lifelong contract, and grossly underperform investment-wise. The monthly premium amount is often 10x (or more) the cost of a term life policy too!

Universal Life Insurance

Like whole life insurance, universal life insurance is also a type of permanent life insurance. It builds cash value as well, which you can borrow from or withdraw.

However, universal life insurance comes with added flexibility. You can adjust your monthly premium, adding to or drawing from that cash value. Similar to whole life insurance, these universal life insurance policies also come with a hefty price tag!

Flexibility does sound nice. But again, we highly advise against mixing investment and insurance products. You are better off paying for a cheaper term life insurance policy and investing the rest of your money elsewhere to build wealth at a faster rate.

Variable Universal Life Insurance

These are the most complex policies, with even higher monthly premiums. Variable Universal Life Insurance is similar to regular UL, but they offer more investment control. You get to choose from a number of investment funds and turn your small cash-value into a mini portfolio.

But while this sounds cool and you might think you can grow cash value faster, it comes at a cost. Not only do you pay higher premiums for the privilege of control, you pay higher fees and commissions to fund managers and advisors. These might seem small on a monthly basis, but they really handicap your ability to sock money away for the future.

Again, insurance and investing don’t mix well. Your nest egg grows faster if you pay no fees and just invest in simple index funds inside your tax-advantaged accounts or in a brokerage account.

In short, term life insurance is the bees knees, and the superior choice for almost everyone to buy. And anyone else who tells you differently is likely making a commission from selling you a policy. Don’t fall for it.

Don’t Forget the Main Purpose

Remember, the most important (actually the only) reason you might need to buy a life insurance policy is to ensure that if you die unexpectedly, anyone who depends on you financially will be able to get by without severe financial constraints.

Basically, life insurance functions a bit more like income insurance. It prevents your death from being a total financial armageddon for your family.

Life insurance is not an “investment” product. It’s there to cover specific financial costs and prevent a large money crisis if you die.

How to Buy Life Insurance:

Now that you understand the true purpose of life insurance, and why buying a cheap term policy is your best option, here are the steps you can follow to successfully purchase life insurance coverage.

Step 1: Decide if you even need life insurance

Do you even need a policy at all? This answer is quite easy to figure out.

If you have someone who depends on your income to survive, like children or a spouse, you need life insurance. If you’re the breadwinner, you are like a single point of failure, and if you die your family would really scramble to make ends meet.

On the flip side, if you’re single and don’t have anyone who depends on your income, you do not need to buy life insurance. You dying (although it would be really sad) wouldn’t be a financial burden on anyone, so no money is really needed.

There is one exception to the rule, and that is, drumroll please… non working spouses! While their families may not rely on their income, they rely on them in many other ways. Stay at home parents and spouses often do hours upon hours of unpaid household work. Cleaning, cooking, shopping and caring for families saves a household tens of thousands of dollars every year.

Should a stay at home parent pass away, their family would lose all of that household help. Hiring someone to assist with these household responsibilities could cost thousands of dollars every month. That’s why a non working spouse will still need to buy a life insurance policy.

Related: How to combine finances with your spouse

Step 2: Decide how much coverage and time you need

Now we’ll need to crunch the numbers and see just how much coverage you should get. Having too small of a policy amount would still hurt your family if you die. But having too much coverage means the policy is more expensive than it needs to be.

It’s tempting to just pick a nice round number (like $5 million) and call it a day. But, remember that the need for life insurance shrinks as your nest egg grows bigger in life. More wealth = less coverage needed.

Finding out exactly how much life insurance you need to buy is pretty simple. Just subtract your current net worth from the amount of money your family would need to be financially independent. We call this your “FI Number,” or Financial Independence Number. For example, if your net worth is $500,000 and your family’s FI number is $2M, you need $1.5M in life insurance coverage.

If you don’t know your FI number or your net worth, don’t panic. We’re going to show you how easy it is to calculate both!

How to calculate your FI number

Calculating your financial independence number is easy, though it may take some time and effort. Your financial independence number is roughly 25 times your annual spending. This means that following the 4% rule, you could theoretically withdraw 4% of your investments each year and never run out of money.

So, if your family spends about $60,000 each year, your FI number would be $1,500,000. Once you achieve this number, you and your family would no longer be dependent on income, meaning you no longer need insurance. When you reach financial independence, you are basically self-insured.

To calculate your own FI number, spend some time looking through your bank and credit card statements. It can be helpful to take the average spend over the past few years so that big expenses like home and car maintenance don’t skew the numbers. Then, just multiply your annual expenses by 25. Boom. You’ve got your FI number.

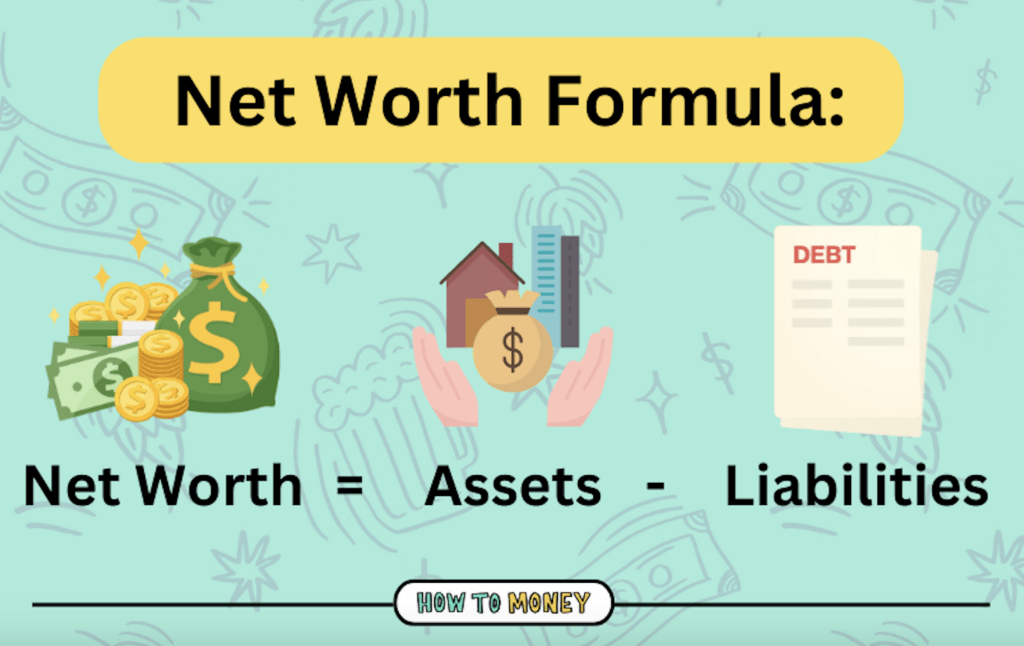

How to calculate your net worth

Luckily for those of us who struggled in math (🙋♀️), calculating your net worth is also very straight forward. The calculation for net worth is as follows:

Net worth = assets – liabilities.

Your assets include things you own with significant value, like your cash, investment accounts, or home equity. Liabilities include your debts, like a mortgage, student loans, or credit card debt. It’s that simple!

**If you currently have a net worth of $0 (or you are in debt), you’ll need quite a large policy. Figure out how much your family would need to be financially free without you, and that should be your policy amount. Oh, and learn to invest ASAP. Your net worth won’t grow on it’s own.

How long should your policy term be?

Your life insurance policy should be for the number of years in which it will take you to reach financial independence. This can generally be determined by calculating your savings rate.

You can use a simple calculator, like this one from NetWorthify. Typically, a 20-30 year term insurance policy works well, because if you have children it will last until they are grown up and independent.

So, in summary, you need coverage that will last you until you reach financial independence. To determine the amount of coverage you need, just subtract your net worth from your FI number.

If you’re young with not much savings, choosing a 30 year term doesn’t hurt. If you grow a lot of wealth and don’t need a policy anymore, you can cancel it at any time and stop paying premiums. Or, if it takes a little longer and you’re reaching the end of your policy, you can always start a new term or possibly extend your old one.

Use “Laddering” if You Need More Coverage

Sometimes, your coverage needs change as time goes on. For example, if you purchased your policy in your 20s or early 30s when you only had your spouse depending on you, you might realize you need more coverage when you’re in your 30s and 40s with multiple kiddos and a larger salary.

If you find yourself in this boat, it doesn’t mean that you need to ditch your current (and likely cheap!) policy. Instead, you can use a “laddering strategy” by purchasing another term life insurance plan that overlaps with your current one.

You can also use this strategy to “create your own” term life insurance that provides changing coverage over the years. For example, you could buy three $500,000 term life insurance plans with 10, 20, and 30 year expiration dates. Then, you’d have $1,500,000 in coverage for the first 10 years, $1,000,000 for the next 10 years, and $500,000 for the last 10 years. This can be a great strategy for someone who is pursuing financial independence, and will need less coverage as they continue to grow their net worth.

Step 3: Shop around for rates

Now that you know exactly what you’re looking for, it’s time to start shopping for rates. Thanks to the internet, finding the best rates for insurance is super easy!

Most life insurance companies will be able to give you a quote online. However, if you want to shop and compare a bunch of different companies all at once, you can use a free tool like Policygenius.

While you probably head to Costco when you need to stock up on bulk food products, or when you’re craving one of those famous Costco hot dogs, Costco is also in the life insurance game! Costco members can get a personalized quote for their term life insurance policies online.

And of course, the major insurance players, like Progressive and Aflac will also allow you to receive and compare quotes online.

Just type in your age, personal info, how much coverage you need and your desired term, then it’ll spit out a bunch of policy options.

Once you find the best quote, make sure to do extensive research on the company before moving forward with your application. Read customer ratings and reviews to ensure you will have a good experience with your insurer going forward.

While you’re shopping around, it’s important to pay attention to the financial rating of the insurer. This is to make sure the insurance company is financially sound, because they need to actually be able to pay out the death benefit should you pass away! You can use websites like AM Best, Moodys, or Standard & Poors to view the financial ratings of different insurance companies.

Step 5: Apply for a Policy

Once you’ve made your decision about which insurer you would like to go with, it’s time to finally apply for that insurance. Follow the insurer’s procedure for filling out the application. They will ask you questions about your age, income, and health history.

In some cases, you might need to have a medical exam to have your policy approved. The medical examiner will come to your home in most cases, and the exam will take between 15-45 minutes. It’s likely that during this exam you’ll have your blood taken for blood and drug tests. They will also take your blood pressure, height, and weight. However, some life insurance policies don’t require any exam at all when you buy them.

Step 6: Review and purchase the plan

Once you are approved for your insurance plan, make sure you go ahead and read all the boring fine print. If you have trouble understanding the language, feel free to call up your potential insurer and ask them to explain. It’s what they’re there for!

If everything looks agreeable, go ahead and purchase the plan. The process will vary from insurer to insurer, so just follow their instructions to finalize your life insurance plan.

Step 7: Choose your beneficiary

Now that you’ve purchased your life insurance plan, you’ll need to pick your beneficiary. This is the person who will receive the payout should you die during the policy term.

Remember, you’ll want your beneficiary to be financially responsible. They’re the one that has to manage the household finances when you’re gone. For most folks the slam dunk choice is their partner or spouse.

Most policies have the ability to name multiple beneficiaries. To do so, you’ll just need to specify what percentage of the death benefit will go to each person.

Naming a minor as your beneficiary can be tricky. For example, if you are a single parent, you may want to give all the money to your child. However, if you die before they turn 18, the insurer may not be able to pay out the death benefit, and instead a probate court would decide on an adult custodian to manage the funds until the child is legal age. If you don’t have a will, things could go wrong if money is managed by the wrong hands.

To avoid any headaches, think carefully about who your beneficiaries should be.

And another piece of advice: Coach your beneficiary and tell them about your policy. Teach them how you want the money used and spent so there is less chance of mismanagement.

Step 8: Set Up Autopay

Failing to pay the premiums for your term life insurance policy can result in your coverage being terminated. We get it. Sometimes life happens, and paying a bill or two may slip your mind. That’s why it can be helpful to set up autopay!

Fortunately, most term life insurance policies have level premiums, meaning they stay the same throughout the entire duration of your policy. It can be helpful to set up automatic payments because you know the exact amount each month or year. Autopaying helps ensure your policy stays active, and it also simplifies your finances!

Real Life Example:

Charlie just got married last year and he and his wife Helen are expecting their first kid. Because his wife and child will depend on his income going forward, he decides that it’s time for them both to buy term life insurance policies.

Charlie makes $85,000 each year and Helen makes $90,000. Because Charlie and Helen both work, they believe they will reach financial independence relatively quickly. Their annual expenses are around $70,000 each year, so they will need $1,750,000 to become financially independent. They have $100,000 saved currently, and together, they invest $4,500 each month, meaning they will hit their financial independence goal within 15 years.

Knowing this, they decide to each buy term life insurance in the amount of $1.65 million with a 15-year term. They use Policygenius to shop around for an insurance company, and when all is said and done, Charlie finds a policy for $218 and Helen finds a policy for $190 annually. They purchase the policy after researching the financial ratings for their insurer, and name each other the beneficiary on their policies.

For a mere $34 a month, Charlie and Helen are both covered if the other one dies. And if they both die, their baby is named as a contingent beneficiary, getting the death benefit for both policies.

Common Life Insurance FAQs:

Purchasing a life insurance policy can be confusing. That’s why we’ve compiled some of the most commonly asked questions most folks have when it comes to insurance!

At what age should you buy life insurance? Should I get life insurance in my 20s to get lower premiums?

It’s not about a particular age. You only need life insurance when someone else depends on your income to survive, like a spouse, children, or other family members. While premiums can be lower if you apply for a policy at a younger age, it’s better to wait until you actually need a policy to get one. You’ll come out on top if you invest the money you would be paying towards those premiums in a tax advantaged retirement account.

For example, if your life insurance premiums were to cost you $220 per year at age 30, and $330 at age 40, the difference you would pay in those premiums over the 20 year term would be $2,200. If you invested that money you would have been paying into your life insurance policies from age 30 to 40, your investments would be worth around $3,301, which more than covers the difference.

Do kids need life insurance?

Despite some of the crummy ads you might see the answer is no. That’s because nobody is dependent on their income. While losing a child would be incredibly sad (and the thought of having millions of dollars to cheer you up is comforting) the truth is that taking out a life insurance policy on your child is wasting money that could be used to help them get ahead financially!

How much does term life insurance cost?

Term life insurance is cheap, leaving you with few excuses not to get it if someone depends on you for financial support. A 20-year term life insurance policy will typically cost between $200-300 annually depending on your age and health history.

I have life insurance from my employer. Is that enough?

Almost never. Employer life insurance does not typically provide you with enough coverage. On average, employer sponsored life insurance is worth the equivalent of your annual salary. As we discussed earlier, you’ll likely need far more coverage than that. Furthermore, your employer life insurance will be terminated should you leave your job or get laid off. You’ll want to purchase a plan that follows you no matter where you work.

What if you can’t self insure at the end of your term life insurance?

Sometimes things don’t go according to plan, and you may not reach financial independence by the date you planned. In that case, many term life insurance plans allow you to request to renew or buy an extension to your term.

What questions should you ask when buying life insurance?

Buying life insurance comes with a lot of intricacies. So here is a little cheat sheet of questions you should ask when you decide which life insurance plan is right for you.

- Do I really need life insurance?

- How much life insurance do I need?

- How long will it take me to be able to self insure?

- Is the prospective insurance company financially stable?

- Are there any exclusions that would prevent my beneficiary from receiving the death benefit?

Remember, if you are speaking to a financial advisor and they are recommending anything other than Term Life Insurance, they are leading you astray. People selling Whole, Universal, or Variable life insurance policies are salespeople, not financial advisors.

Why is life insurance cheaper for women?

Generally speaking, life insurance costs less for women. In fact, they pay an average of 24% less for health insurance than their male counterparts. This is because statistically speaking, women have longer life spans than men, meaning they are less likely to die during the duration of the policy. Increasing the cost of life insurance for men is the insurer’s way of hedging against risk.

That being said, it’s not just your sex that affects policy costs. There are a lot of different health factors that could increase (or reduce) your premiums.

Can You Back Out of Term Life Insurance?

Sometimes, your situation may change causing you to no longer need life insurance. Maybe you’ve become able to self insure earlier than you thought, or your domestic situation has changed. Luckily, canceling term life insurance is super easy.

You can call or write to your insurance company to let them know you will be canceling your policy. Some companies may even allow you to terminate your coverage online. Or, you could just stop paying your premiums and they will cancel it for you!

Does Term Life Insurance Lose Value?

With most term life insurance policies, your death benefit will be the same throughout the duration of your term. This means your beneficiary would receive the same amount of money if you died in your first year of your policy, or your last year! When in doubt, ask your insurer for more details on your policy.

What are the different kinds of term life insurance?

When shopping around for term life insurance, you may come across a few different options. Here is a cheat sheet to understand the different term life insurance offerings:

- Level Premium- This is the most common type of term life insurance people buy. Under level premium policies, the amount you pay each month will remain the same throughout the duration of your coverage.

- Yearly Renewable- This option allows you to purchase yearly coverage, with the option to renew it at the end of each year. Each year when you renew, your premiums will be raised. Since you can cancel a level policy at any time, it is often preferable to stick with a level premium plan. At the end of a 10-30 year period, your premium would be much higher with a yearly renewable policy than a level premium policy.

- Guaranteed Issue- These policies are easy to get and don’t require a medical exam. However, your premiums will likely be higher as the insurance company will consider you a higher risk, assuming you likely have health issues that would prevent you from applying to a level premium plan.

- Return of Premium- This type of policy allows you to get some of your premiums returned to you if you do not use the death benefit. While this may sound appealing, the premiums are much higher than level premium insurance plans.

The Bottom Line:

No one wants to think about the end. But unexpected deaths happen every day, so it’s important to buy the correct life insurance to protect your loved ones should the worst happen. Purchasing term life insurance can provide yourself, and your family with peace of mind without breaking the bank.

To buy a term life insurance policy, just figure how much coverage you need, the term you need it for, and which beneficiaries you trust. Using an online comparison tool like PolicyGenius will help speed up the process and get you the best deal.

So, if you need life insurance, what are you waiting for!? Go and purchase that policy!

Related Posts: